Documentation Index

Fetch the complete documentation index at: https://docs-preview.infinifi.xyz/llms.txt

Use this file to discover all available pages before exploring further.

This is the full infiniFi whitepaper. For a high-level overview, see the Developer Summary.

Abstract

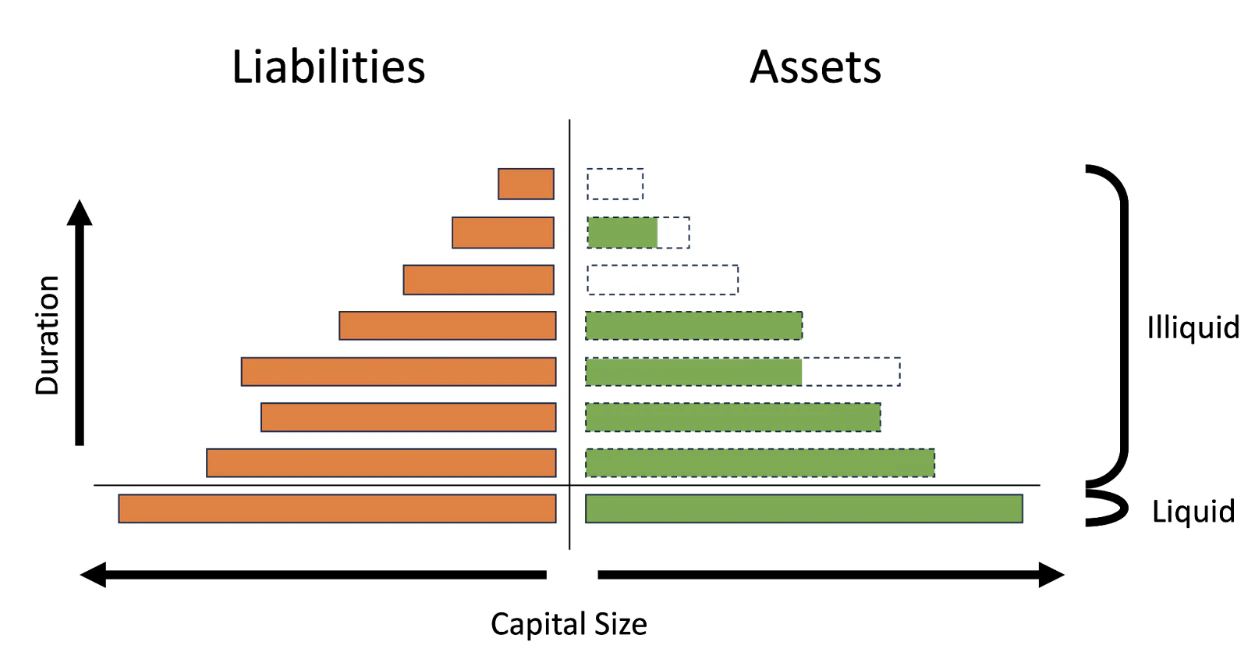

For the vast majority of history, the world’s financial capital has rested on a flawed foundation. Today, nearly all modern government treasuries and private financial institutions rely on fractional reserve banking. Banks use past behavior to predict how much of their customers’ deposits to keep on hand while lending out the rest to secure greater returns. This can lead to greater capital efficiency and economic expansion in the regions they serve. However, fractional reserve banking also creates duration gaps — a mismatch between the average maturity of a bank’s liquid liabilities and illiquid assets — which can lead to insolvency if enough depositors attempt to withdraw their money at once. To account for those duration gaps, banks must efficiently manage their balance sheets, effectively model cash outflows, and appropriately handle coordination failures that could lead to bank runs. However, they have imperfect solutions for doing so, relying on reactive lookback models and centralized planning models that misalign incentives between them and their depositors. We propose InfiniFi, a fractional-reserve stablecoin powered by a self-coordinated, duration-matching autonomous balance sheet to directly measure market sentiment and address the problems posed by duration gaps. This depositor-directed system decentralizes how assets are allocated, giving individual depositors choices based on their specific risk, duration, and liquidity preferences.1.0 The Fracturing of the Fractional Reserve System

Fractional reserve banking has existed for centuries. It relies on the fact that depositors do not generally ask for all of their money back at once. That means shrewd bankers can lend out a significant portion of those deposits and generate high returns, so long as they keep enough cash on hand to cover expected withdrawals. This increase in capital efficiency comes at a cost. The vast majority of depositor obligations held by banks (their liabilities) are fully liquid (90%) and may be redeemed at any point in time. However, the illiquid assets held by banks have a duration associated with them that must pass before they reach maturity. The mismatch between these zero-duration liabilities and these positive-duration assets is termed the “duration-gap” and serves as the core problem that most banking infrastructure has been built to address.1.1 The Misaligned Incentives of Centralized Balance Sheets

The top-down approach that banks utilize to address laddering results in the creation of perverse incentives. As employees are rewarded for producing the best outcomes for their employers, they are encouraged to pursue goals that will provide the best outcomes for the bank, rather than the depositors.1.2 The Limitations of Lookback Models

All banking models suffer from a common flaw: they largely rely on look-back models. Look-back models use historic knowledge to predict what future events will occur. The black-swan events that often precipitate a bank failure are by their nature unpredictable, and fundamentally break the assumptions that go into models of this design.1.3 The Socialized Cost of Coordination Failure

Even banks that are fundamentally solvent may fall victim to a bank run when depositors are uncertain about the health of their investments. A potential liquidity crisis leaves depositors with a prisoner’s dilemma: while it may benefit everyone involved to keep their funds in the bank, there is a strong first-mover incentive for depositors to recover their funds early.2.0 Introducing InfiniFi

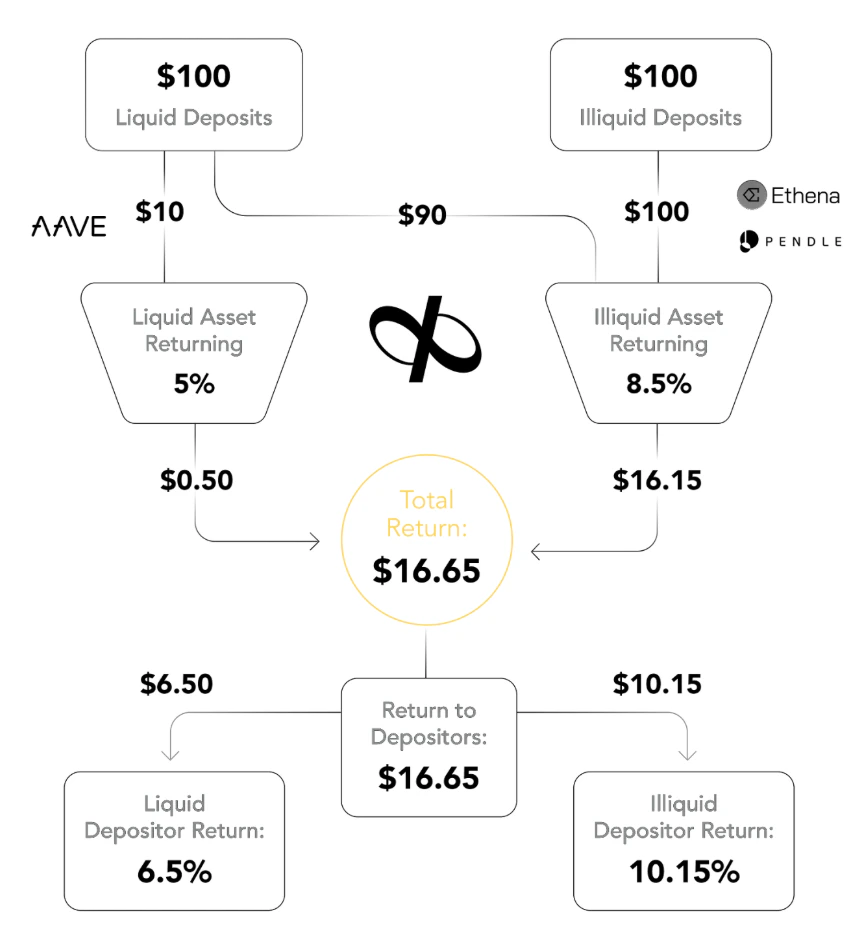

InfiniFi is a self-coordinated, depositor-driven fractional reserve system built to better address the challenges created by duration gaps in traditional banking, aligning incentives while securing greater returns without increased risk regardless of asset class.2.1 How InfiniFi Works

When someone deposits USDC into InfiniFi, they mint iUSD, and that deposit asset is immediately deployed to a trusted set of liquid vehicles. To achieve higher returns, they must bond their iUSD, with depositors self-selecting an unbonding period based on their time preferences. Depositors receive an ERC20 token to represent their bonded iUSD. To incentivize staking iUSD, InfiniFi awards depositors who stake for a longer period of time with a higher weighted-average time-multiplier.

Key Concepts

Tokens

| Token | Description |

|---|---|

| iUSD | Receipt Token - obtained by depositing USDC |

| siUSD | Staked Token - obtained by staking iUSD, provides liquid returns |

| liUSD-xw | Locked Position Token - obtained by locking iUSD for x weeks |

Farms

- Liquid farms → Instant access to principal (e.g., AAVE)

- Maturity farms → Delayed access with higher yields (e.g., Pendle, Ethena)

- Protocol farms → Internal fund movement, no yield accrual

Read the full whitepaper

View the complete whitepaper with all technical details on GitHub.